Embedded Insurance Statistics and Market Dynamics (2026)

Embedded insurance is rapidly reshaping how insurance is distributed, priced, and experienced – moving coverage from a standalone decision to a natural part of everyday digital interactions.

Backed by accelerating adoption, platform-driven distribution, and strong shifts in gross written premiums, the latest market statistics reveal embedded insurance as one of the fastest-growing segments of the global insurance industry.

Embedded Insurance: General Outlook

Embedded insurance refers to insurance coverage that is seamlessly integrated into the purchase flow of a product or service, rather than sold as a standalone policy.

These embedded insurance offerings are typically delivered at the point of need – when customers are already engaged in a digital transaction – making protection contextual, easy to understand, and frictionless to activate.

For customers, this model simplifies access to relevant insurance offerings; for distribution partners, it creates incremental revenue and deeper engagement; and for traditional insurers, it opens scalable access to new customer segments through digital distribution. As APIs, real-time data exchange, and automated underwriting mature, embedded insurance products are becoming a core mechanism for increasing insurance penetration and modernizing distribution strategies.

Consequently, the embedded model is no longer experimental – it is increasingly viewed as a foundational pillar of future insurance ecosystems, as highlighted across every major embedded insurance market report.

Key market indicators illustrate both the scale and velocity of this shift:

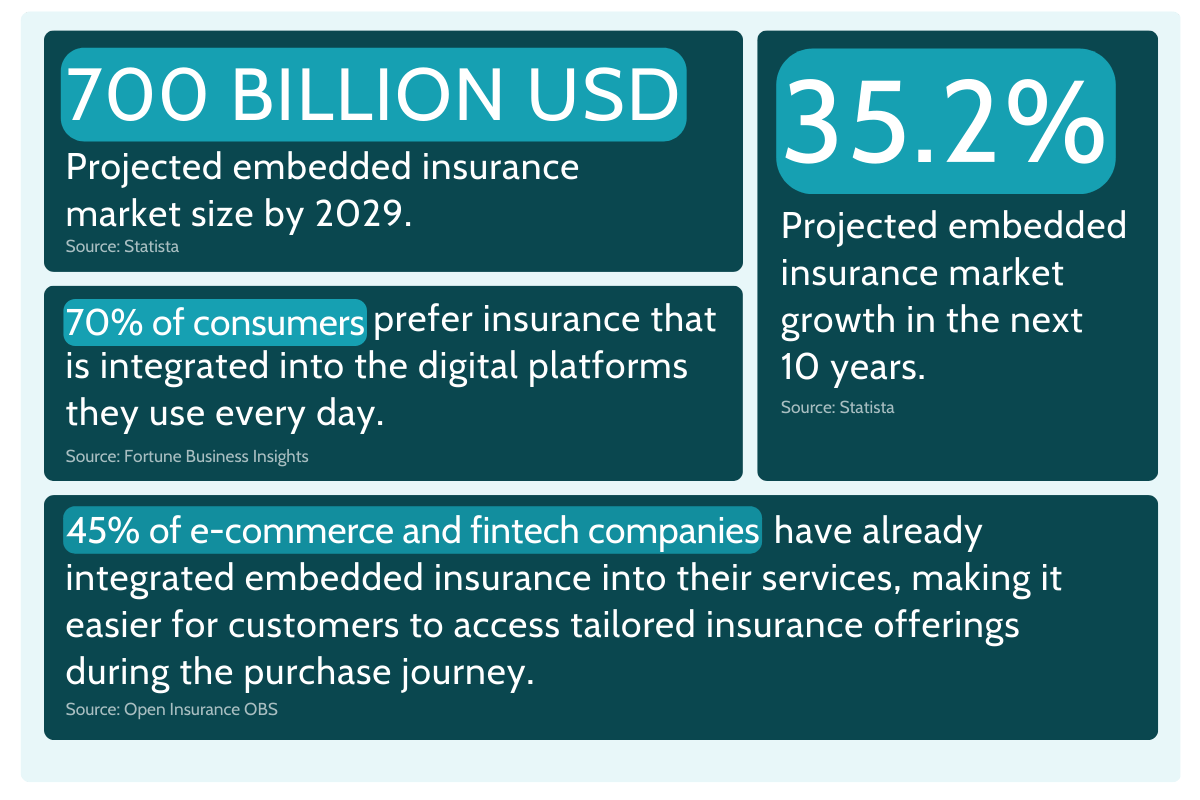

- Total market value: The global embedded insurance market is projected to grow from $176.35 billion in 2026 to $1,464.42 billion by 2034, up from $143.88 billion in 2025, reflecting accelerating adoption across industries. (Fortune Business Insights)

- Property & Casualty momentum: Embedded P&C insurance could exceed $700 billion in gross written premiums by 2030, accounting for roughly 25% of global P&C premiums, signaling a structural redistribution of risk placement. (FinancialIT)

- Penetration trajectory: Strategic sizing models estimate embedded insurance at less than 1% of total insurance today, expanding to around 5% by 2027 and 15% by 2032, with higher concentration in modular, short-duration embedded insurance products. (SwissRe)

- Product mix evolution: Electronics protection led the market in 2025 with a 44.74% share, while IoT-driven micro auto insurance – enabled by real-time data and usage-based pricing – is forecast to grow at a 33.87% CAGR through 2031. (MordorIntelligence)

- Regional growth dynamics: Embedded insurance in Asia is projected to reach approximately $270 billion in gross written premiums by 2030, with a significant portion driven by premium volumes shifting away from agent-led models toward platform-based digital distribution, according to McKinsey. (FintechFutures)

Embedded insurance market size valuations, and growth rates

Following the broader market outlook, size and growth indicators reinforce the view that the embedded insurance market is not only expanding rapidly, but doing so at a pace that significantly outstrips the wider insurance industry. While traditional insurance channels continue to grow in low single digits in most mature markets, embedded distribution is scaling at multiples of that rate, driven by accelerating consumer demand for simple, contextual protection and by the growing ability of digital platforms to integrate insurance seamlessly into their core journeys.

From a revenue perspective, global embedded insurance revenues reached $56.98 billion in 2022 (Global Embedded Insurance Business and Investment) and are projected to rise to $161.60 billion by 2029, reflecting sustained momentum across both P&C and selected life insurance use cases.

Alternative market sizing models, using a gross written premium lens, estimate the market at $213–355 billion in 2023, with forecasts converging toward approximately $1.1 trillion in GWP by 2033. While the range varies depending on definitions and product scope, every major embedded insurance report points to the same conclusion: embedded distribution is transitioning from a high-growth niche into a core insurance channel.

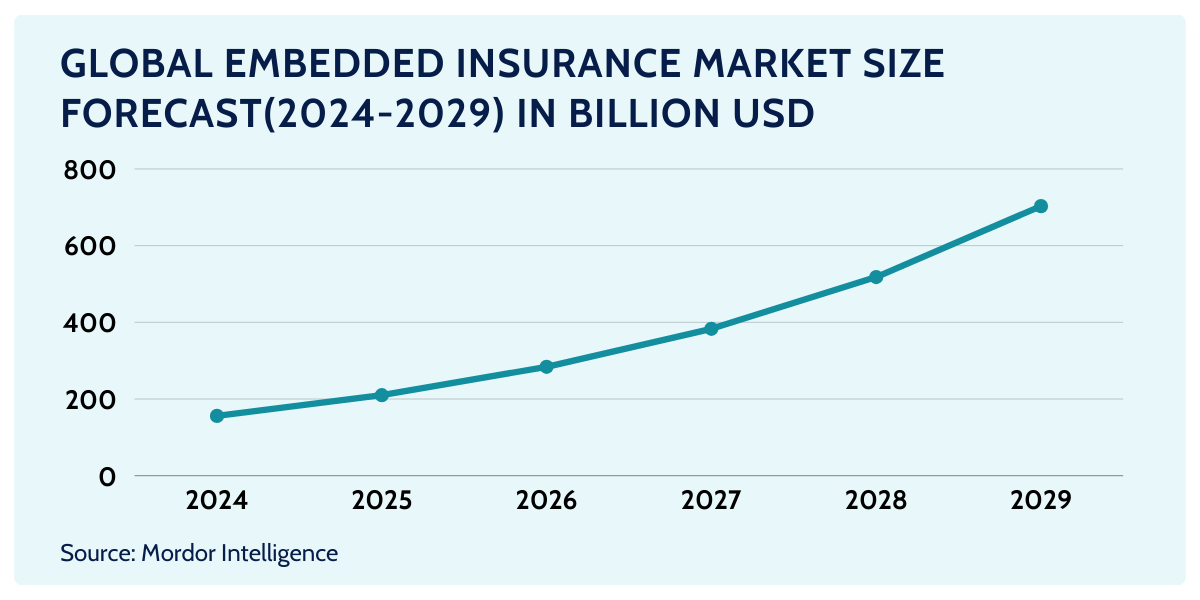

Shorter-term forecasts underscore this acceleration. The embedded insurance market is expected to grow from USD 18.09 billion in 2026 to USD 68.12 billion by 2030 (MordorIntelligence), representing a 30.37% CAGR as coverage migrates from stand-alone policies to “invisible” protection bundled into everyday digital experiences. This growth is being fueled by increasingly sophisticated embedded insurance solutions, including real-time underwriting, usage-based pricing, and modular coverage that aligns tightly with customer intent at the point of purchase.

Most notably, embedded distribution is on track to capture up to 15% of total insurance flows by the early 2030s (Open & Embedded Insurance Observatory), a shift unmatched by any other established insurance sales funnel. Compared with agents, brokers, bancassurance, or direct-to-consumer models, embedded insurance offerings represent the most dynamic growth vector in the market today – reshaping how insurers reach customers, how products are designed, and how value is created across the digital economy.

Market size by year and region

A regional breakdown of revenues further illustrates strategically important the growth of the embedded insurance market has become.

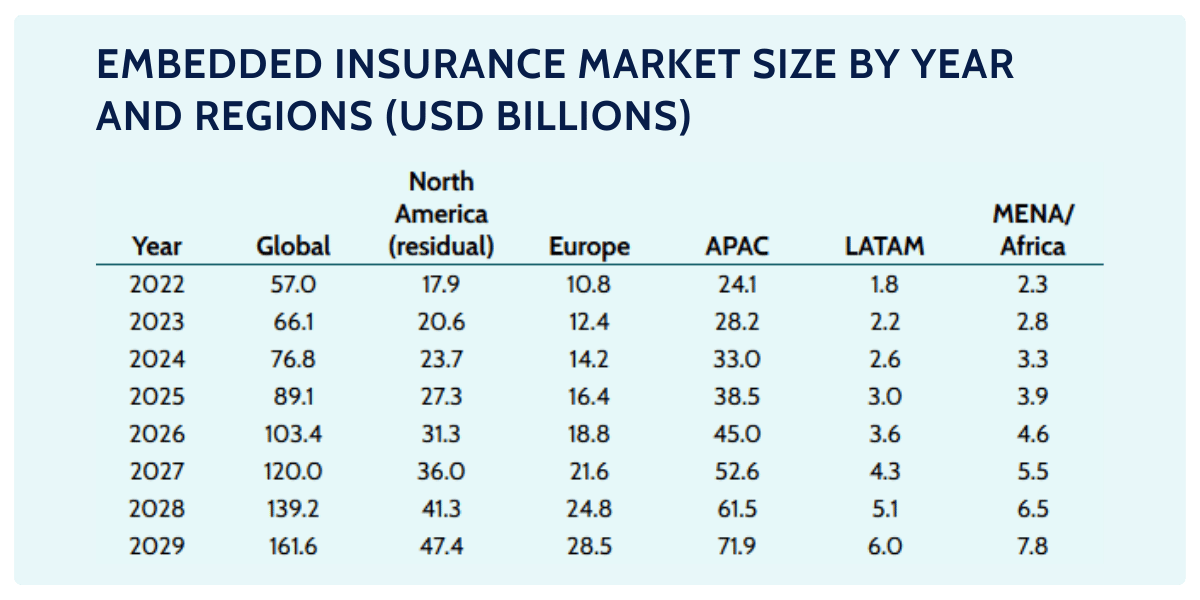

According to consolidated estimates from the latest embedded insurance market report, global embedded insurance revenues are projected to nearly triple from $57.0 billion in 2022 to $161.6 billion by 2029, but this expansion is being driven disproportionately by Asia-Pacific and other high-growth regions. APAC alone is expected to grow from $24.1 billion in 2022 to $71.9 billion by 2029 (PRnewswire), accounting for almost half of total global growth in absolute terms.

By contrast, North America and Europe show strong but more linear growth patterns.

North America’s embedded insurance market size increases from $17.9 billion to $47.4 billion over the same period, while Europe grows from $10.8 billion to $28.5 billion, driven largely by retail, travel, and automotive use cases. However, the most striking relative momentum comes from emerging markets beyond APAC. LATAM and MENA/Africa, while smaller in absolute terms, more than triple their embedded insurance revenues between 2022 and 2029 – signaling that embedded distribution is often leapfrogging traditional insurance infrastructure entirely in these regions.

Taken together, the regional data underscores a key structural insight: the embedded insurance market is not expanding uniformly, but rather following digital adoption curves and platform density.

Embedded vs Traditional Channels

Open-source analyses consistently point to embedded insurance offerings absorbing volume from agency, bancassurance, and branch-led sales, rather than merely creating incremental demand.

In Asia, for example, McKinsey estimates that 66% of embedded insurance growth is driven by gross written premiums migrating out of traditional channels and into embedded distribution. This highlights a redistribution of value driven by superior timing, relevance, and customer engagement at the point of transaction.

A broader global perspective reinforces this trend. According to the Swiss Re–Embedded Finance outlook, “EI 2.0” could account for roughly 16% of total global insurance distribution by 2032 (SwissRE), equivalent to around $1.5 trillion in gross written premiums, assuming a total global market of approximately $7 trillion. In selected Property & Casualty segments, embedded distribution could approach 30% market share, taking volume primarily from tied agents and physical branch networks.

These estimates align with global market calibration data from International Association of Insurance Supervisors, which reported $1.75 trillion in gross reinsurance premiums in 2024, representing about 23% of total global premiums – implying a total global GWP base of roughly $7.6 trillion (IAIS).

While P&C dominates today, embedded solutions are increasingly being explored for modular life insurance policies, credit-linked protection, and subscription-based coverage models.

As key companies across mobility, retail, and financial services deepen platform integration, embedded insurance is becoming a primary interface between insurers and end customers – reshaping how insurance is discovered, purchased, and perceived.

Product-Line Mix Snapshots

A closer look at product mix provides additional insight into how embedded insurance operates in practice.

In Europe, a representative market snapshot shows travel insurance accounting for 33.65% of the embedded insurance market in 2025 (MordorIntelligence), reflecting its natural fit with digital booking flows and high-intent purchase moments. Distribution is overwhelmingly digital: online platforms generate 93.10% of embedded insurance revenues, underscoring the central role of e-commerce platforms as the dominant access point for embedded insurance offerings.

Beyond travel, electronics protection and device insurance are consistently flagged as fast-growing lines, driven by rising consumer expectations around consumer protection, instant claims handling, and replacement services.

These products benefit from tight integration with checkout flows, pricing transparency, and immediate activation – features that traditional insurance channels struggle to replicate at scale.

Embedded Insurance Sector Distribution Mix Overlook

Beyond channel disruption, the embedded insurance landscape is also defined by a rapidly evolving sector mix that reflects where seamless coverage delivers the most immediate value. Adoption is strongest in sectors where insurance can be tightly coupled with the core transaction, supported by real-time data, and delivered through online services with minimal customer friction.

Key embedded insurance placements and sector dynamics include:

- Electronics protection and device insurance: The largest embedded line to date, accounting for 44.74% of market share in 2025, driven by high-frequency retail transactions and clear value propositions around replacement, repair, and extended warranties at checkout.

- Micro auto and mobility insurance: The fastest-growing segment, with IoT-enabled micro auto insurance projected to expand at a 33.87% CAGR through 2031. Growth is fueled by telematics, OEM-led journeys, and insurance embedded directly into vehicle financing, ownership, and subscription models.

- Online and API-first placements: By distribution method, API-based and digitally native integrations captured 76.38% of the market in 2025, advancing at a 23.35% CAGR through 2031. These placements enable insurers to scale across platforms while maintaining consistent underwriting and pricing logic.

- E-commerce and marketplace ecosystems: By end-user industry, e-commerce platforms and digital marketplaces represented 52.24% of embedded insurance adoption in 2025, leveraging high transaction volumes and strong customer intent at the point of purchase.

- Mobility and automotive platforms: Although smaller in absolute share, this sector recorded the highest growth rate at 28.36% CAGR through 2031, reflecting the convergence of mobility services, data-driven risk assessment, and bundled insurance offerings.

- Digital subscriptions and SaaS services: An emerging category where embedded insurance is increasingly used to protect business continuity, data, and service availability—creating natural entry points for cyber insurance bundled into recurring digital products.

- Financial products and protection add-ons: Credit, leasing, and buy-now-pay-later journeys are evolving into distribution points for modular protection, including payment protection and simplified life insurance cover, delivered as opt-in embedded layers rather than stand-alone policies.

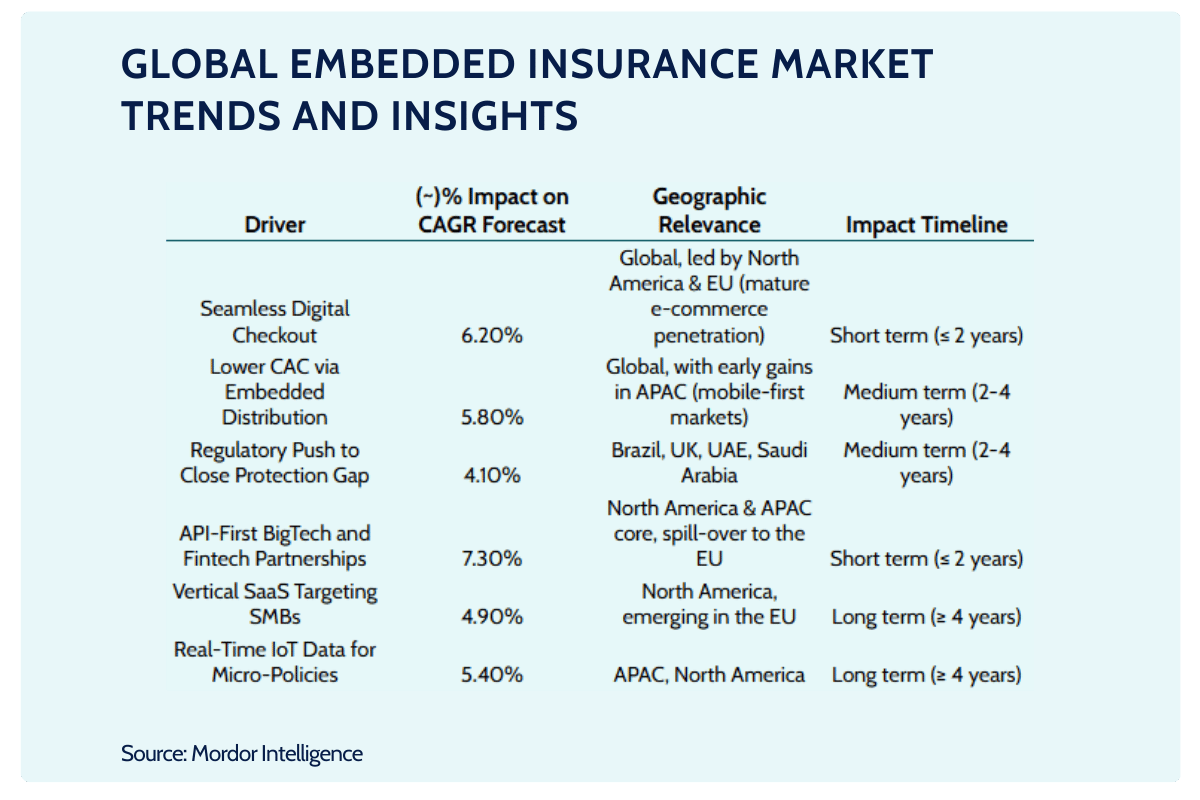

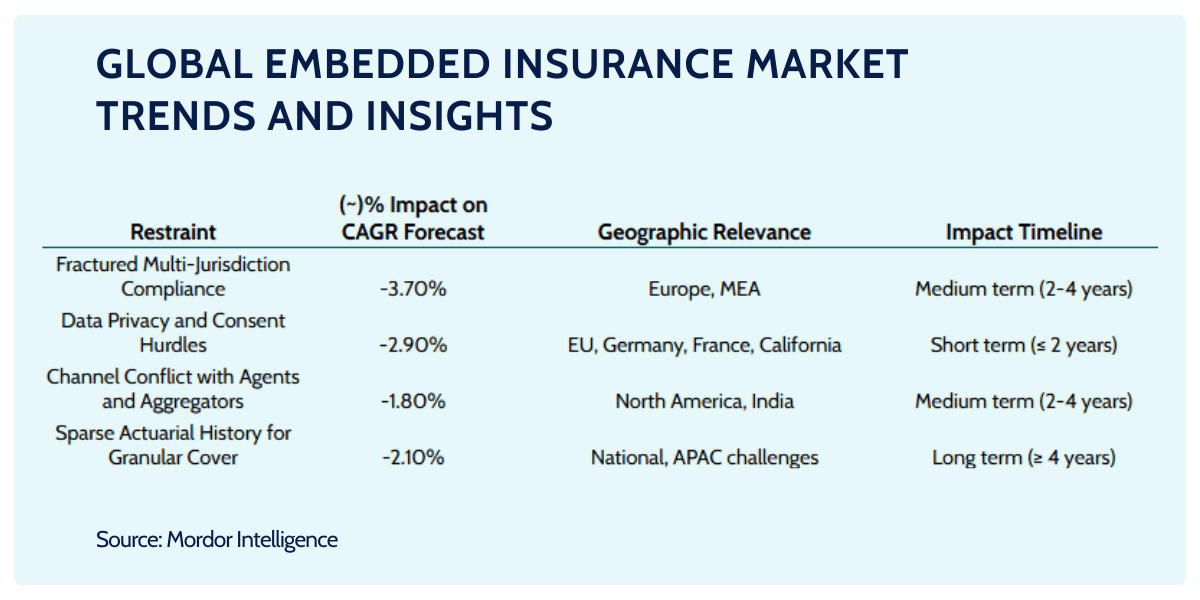

Global Embedded Insurance Market Trends

Across regions, the embedded insurance market is being shaped by a common set of structural trends that point to long-term.

What is emerging is a more mature embedded insurance sector, defined by platform economics, modular technology, and deeper integration into everyday financial and digital experiences.

A defining shift is the rise of embedded insurance as “digital bancassurance 2.0.”

Insurance is becoming a native feature inside banking/fintech journeys (accounts, cards, loans, wealth apps), not a separate “insurance tab” or referral. The bank/fintech becomes the distribution owner (and increasingly the UX owner), pushing insurers toward commoditization unless insurers differentiate through underwriting, claims, and service.

At the same time, API-first and modular productization are dramatically lowering integration cost and time-to-market.

Embedded insurance is shifting from bespoke integrations to lego blocks: quote, bind, payment, policy issuance, endorsements, claims FNOL, document generation, cancellations – exposed as APIs/components that partners can plug into.

Finally, the market is evolving beyond simple add-on warranties toward higher-value lines such as auto, health, and SME insurance, as data availability and orchestration capabilities improve.

It’s a shift from “checkout add-on” to “relationship insurance.”

That pushes embedded models to prove they can handle the hard parts of insurance (claims, retention, regulation), not just distribution.

[Read also: Top 5 Embedded Insurance Providers in 2026]

Rise of AI-driven Functionalities in Embedded Insurance to Boost Market Growth

AI is rapidly becoming a powerful accelerator of embedded insurance adoption.

By automating underwriting, pricing, claims triage, and fraud detection, AI enables embedded insurance solutions to operate in real time – making seamless insurance integration scalable.

How would that look like in practice?

An AI-enabled embedded insurance solution typically operates invisibly inside a digital journey. As a customer completes a transaction – such as purchasing a device, booking mobility, or onboarding with a financial platform – AI analyzes contextual signals in real time and instantly determines eligibility, risk, and pricing. The most relevant coverage is then surfaced as a natural part of the flow, with no separate forms or redirection, ensuring seamless insurance integration. Once accepted, the policy is issued automatically via APIs, and ongoing servicing or claims handling is largely AI-driven, using data inputs to validate events and resolve simple cases instantly.

For traditional insurers, AI lowers the barrier to participating in embedded models by reducing marginal costs and improving risk selection across high-volume, low-ticket products.

For financial institutions and platform operators, it enables more precise offers, smarter cross-sell logic, and better conversion without disrupting the core user experience.

As a result, embedded insurance is evolving into a highly efficient distribution channel, where coverage is context-aware, dynamically priced, and continuously optimized.

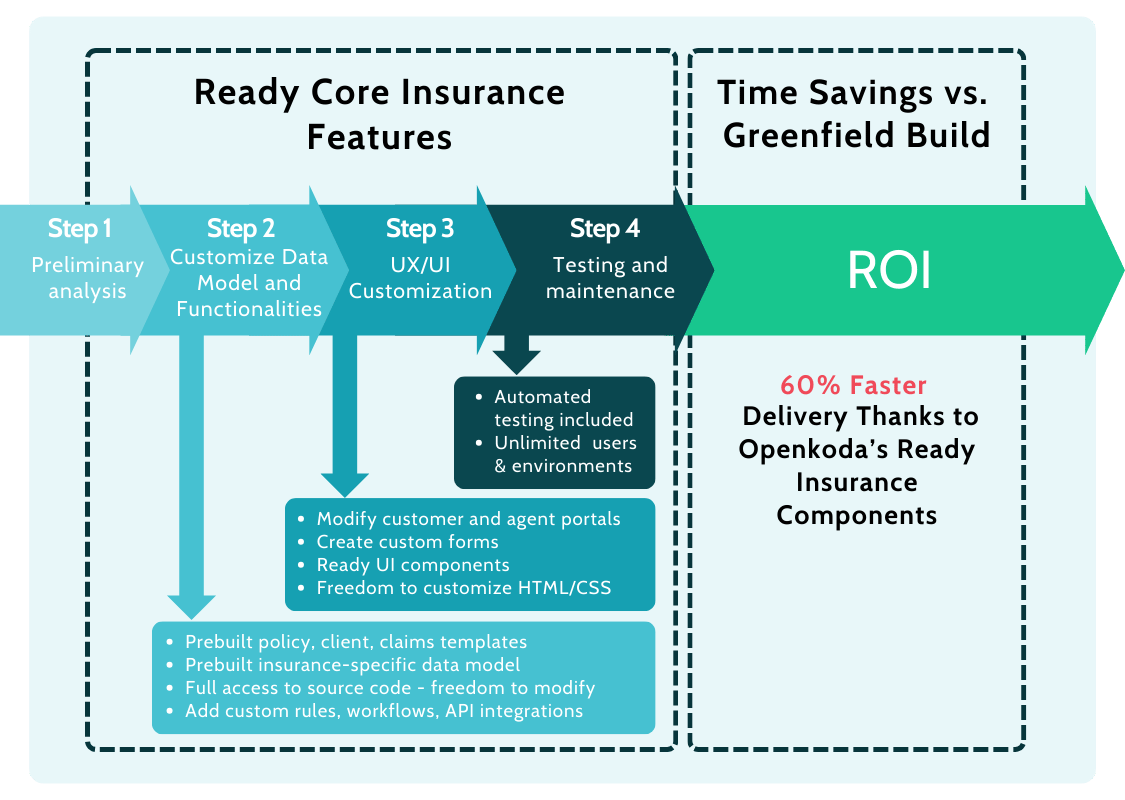

Embedded Insurance Platform Development

At the core of launching scalable embedded insurance products is the right technology foundation – and platforms like Openkoda are designed precisely for that purpose.

Openkoda is an open-source insurtech development platform that enables insurers, fintechs, and digital partners to build custom embedded insurance solutions quickly and without vendor lock-in.

Its modular architecture and ready-to-use building blocks mean companies can design, test, and deploy embedded insurance offerings with seamless integration into websites, apps, or partner ecosystems in a fraction of the usual time.

By reducing development complexity and enabling flexible customization, Openkoda helps both traditional insurers and digital innovators respond to emerging demand and adopt cutting-edge technology without reinventing core systems.

Here’s how designing an embedded insurance for device protection solution typically works with Openkoda:

- Step #1: Define your embedded form structure: Start by outlining the core questions and data points (e.g., travel dates, device details, coverage choices) needed for quoting.

- Step #2: Add product logic and coverage options: Configure dropdowns, coverage tiers, and dynamic fields that reflect your embedded insurance offerings, pulling values directly from your product database.

- Step #3: Incorporate premium calculation: Integrate real-time premium logic so quotes adjust instantly based on user input, enhancing transparency and conversion.

- Step #4: Validate and optimize: Introduce form validation to ensure data accuracy and a smooth user experience that boosts satisfaction.

- Step #5: Embed and launch: Drop the finished form into your website, portal, or platform with a simple snippet – achieving seamless integration with existing digital journeys and backend systems.

- Step #6: Enhance and extend: Once live, you can continually customize and expand the solution—adding new lines, data-driven insights, or integrations with underwriting partners—as your market needs evolve.

&p[summary]=The most important embedded insurance statistics explaining market growth, distribution shifts, and future trends.){kind=link}

{kind=link}